- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

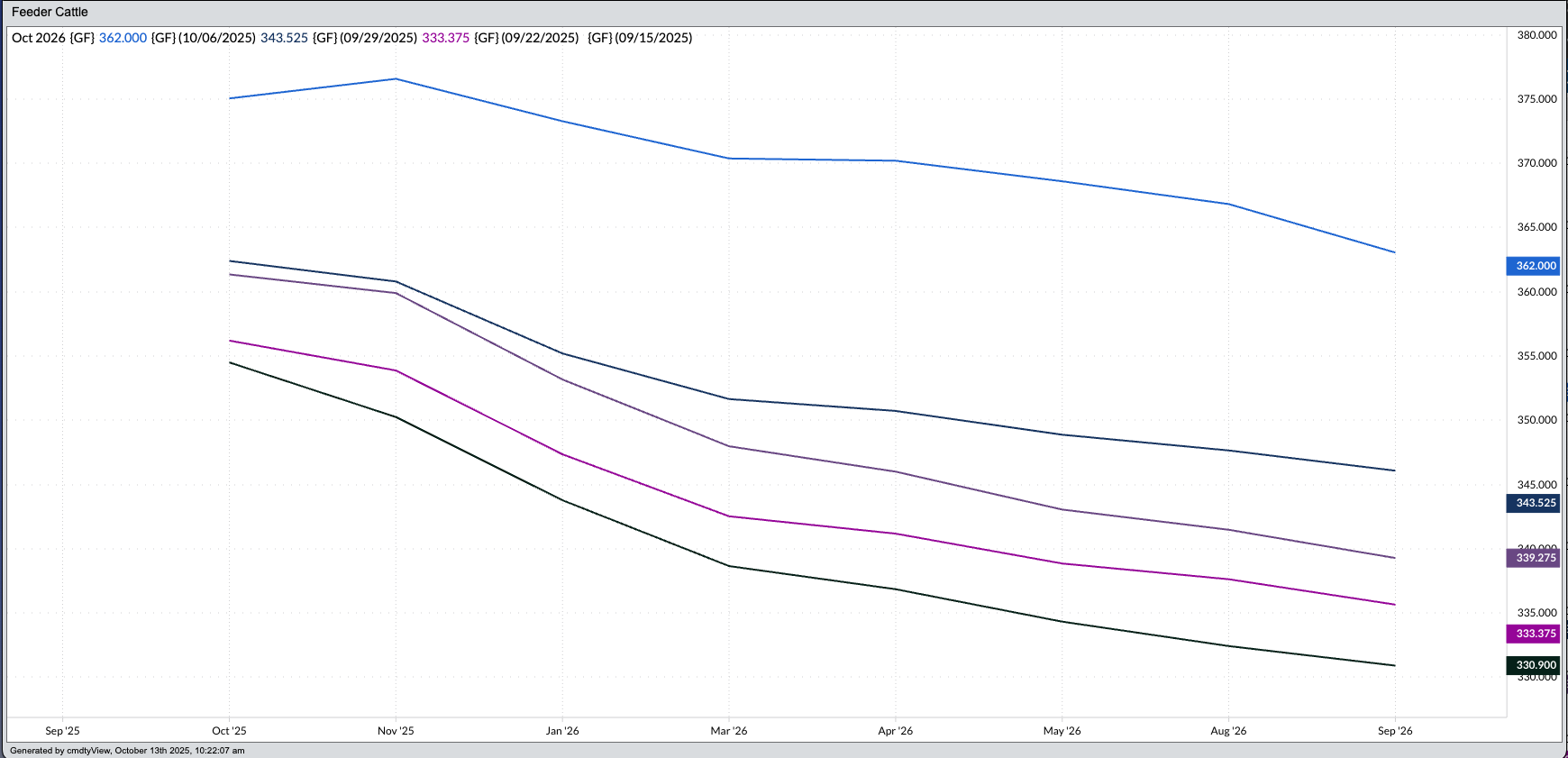

What is the Feeder Cattle Forward Curve Telling Us?

Recent activity in the feeder cattle market has seen nearby contracts lose ground to deferred issues, changing the look of the market's forward curve.

When evaluating any forward curve we have to consider whether the underlying commodity is storable or non-storable.

Based on this, short-term feeder cattle fundamentals remain bullish, despite the recent weakening of the November-January futures spread.

Before the Barn doors were opened Monday morning – meaning the opening bell sounding for the Livestock sector – a friend in the cattle industry sent me a message that turned into the theme of today’s discussion, “Forward curve absolutely getting destroyed on this rally in feeder cattle futures.” This is an interesting subject, and gives us something to talk about while waiting for the next social media missive (misinformation?) from - well, you know.

Let’s start with a definition: A forward curve is a graph showing the price relationship between futures contracts. For storable commodities, there is a natural tendency for deferred contracts to be higher priced than nearby due to storage and interest costs. This is called carry or contango, the former if you trade Grains in Chicago (Minneapolis, Winnipeg, etc.), the latter if your interests lean more toward the New York markets. The stronger the carry/contango, the more bearish the outlook for a market’s real supply and demand situation. When it comes to grains, we can then evaluate how bearish the carry is by comparing it to calculated full commercial carry, but that’s a discussion for another day.

The flip side of the forward curve coin is when deferred contracts are priced lower than nearby issue. This price relationship is called an inverse or backwardation and reflects the situation where merchandisers/end-users are pushing the nearby futures price in relation to deferred to source supplies to fill demand. Again, the stronger the inverse/backwardation the more bullish a market’s fundamentals. The Softs sector has seen one backwardated forward curve after another, the latest being coffee and cocoa. Given Softs, along with Grains, are weather derivatives at heart, and demand markets are few and far between, an inverse/backwardation usually reflects adverse weather reducing supplies.

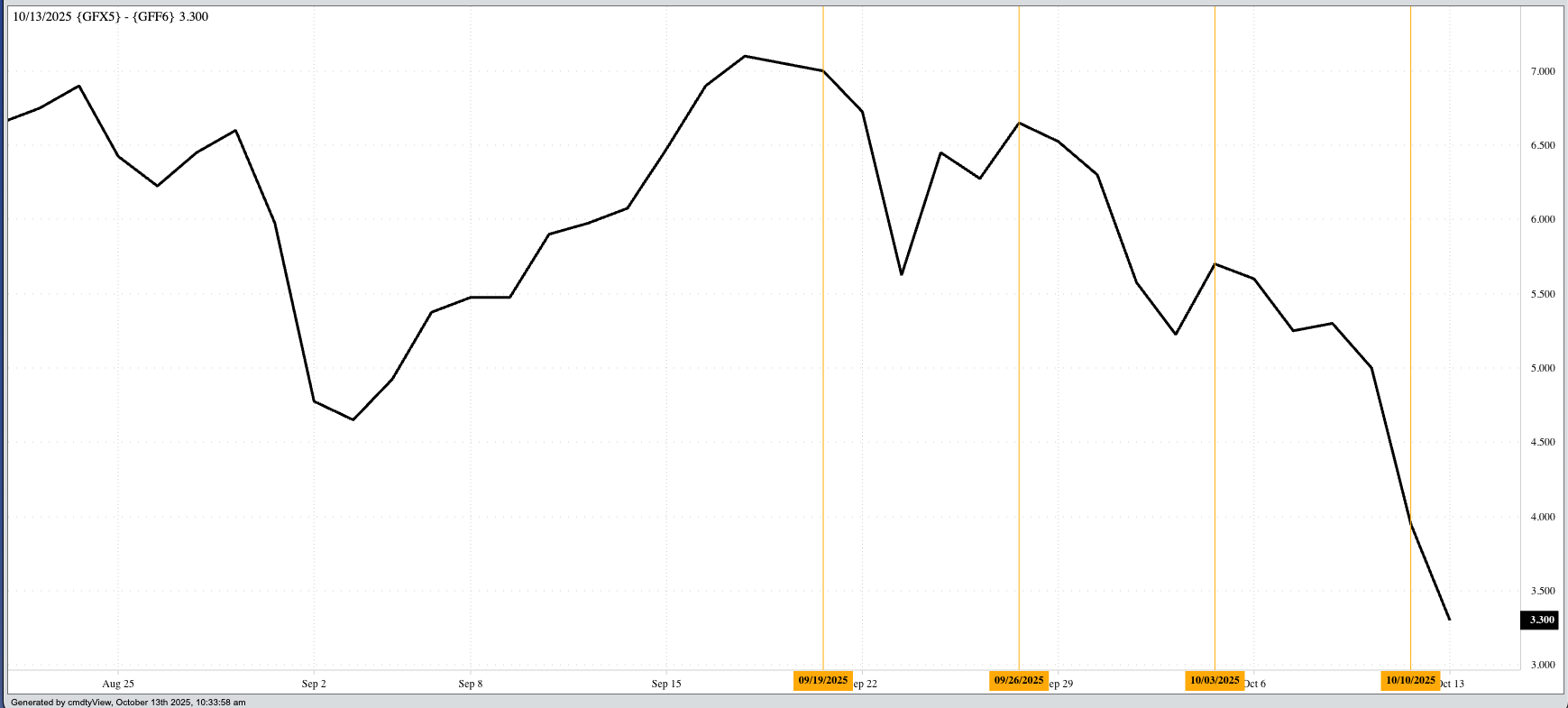

But what about non-storable commodities, like those found in the Livestock sector? Yes, I know we have, or at least had, monthly Cold Storage reports indicating stocks of beef, pork, poultry, dairy, etc., but actual, physical cattle and hogs can’t be stored indefinitely. At some point they simply die. Given this non-storable aspect of the three major markets in the sector – live cattle, feeder cattle, and lean hogs – can we read anything into the forward curves of these markets? I would say no. If we want to understand what the spreads are telling us about supply and demand, I take the current[i] spread (e.g. November 2025-January 2026 feeder cattle) and compare it to what we’ve seen the past five years.

For example, based on weekly closes only, the Nov25-Jan26 spread posted a high weekly close of $7.10 from the second week of August. The previous 5-year high weekly close for that same week was $2.60, with the previous 5-year low coming in at (-$0.50). Fast forward to this past Friday (October 10) and the spread closed at $3.95, dropping $3.15 over the course of 8 weeks but still bullish compared to last week’s previous 5-year high weekly close of $1.525. The bottom line is short-term fundamentals of the feeder cattle market remain bullish.

Can livestock spreads be sharply negative (nearby lower priced than deferred) and still be bullish? Conversely, can livestock spreads show a strong positive price (nearby higher than deferred) and still be bearish? The answer to both is yes. This past summer, the August-October lean hog spread posted a weekly close of $18.10. That sounds bullish, correct? However, it’s previous 5-year low weekly close for that same week was $18.175 meaning fundamentals were actually more bearish than they had been since 2020. On the other hand, the Feb-April live cattle spread recently posted a weekly close of (-$0.875), still a bullish read on longer-term supply and demand given the previous 5-year high weekly close for that week was (-$0.80).

The key is not whether a spread is positive or negative (inverted/backwardated or carry/contango) but whether the underlying commodity is storable or non-storable. Given this, the answer to the question, “What is the feeder cattle forward curve showing us?”, is not much. Instead, futures spreads individually continue to indicate a bullish supply and demand situation. Just not as bullish as before.

[i] My apologies Tony D.

On the date of publication, Darin Newsom did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.