- Market Overview

- Futures

- Options

- Custom Charts

- Spread Charts

- Market Heat Maps

- Historical Data

- Stocks

- Real-Time Markets

- Site Register

- Mobile Website

- Trading Calendar

- Futures 101

- Commodity Symbols

- Real-Time Quotes

- CME Resource Center

- Farmer's Almanac

- USDA Reports

Chubb Limited Stock: Analyst Estimates & Ratings

/Chubb%20Limited%20office%20sign-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Carrying a market capitalization of roughly $108.8 billion, Chubb Limited (CB), headquartered in Zurich, Switzerland, stands as the world’s largest publicly traded property and casualty insurance company. Its footprint spans 54 countries and territories, delivering a wide range of solutions, including commercial and personal property and casualty insurance, personal accident and supplemental health coverage, reinsurance, and life insurance.

Over the past year, shares of CB have experienced a mild decline, lagging the S&P 500 Index ($SPX), which climbed 14.3% during the same period. Year-to-date, the stock remains in a negative territory, failing to match the SPX’s 9% gain.

Even when compared to the broader financial sector, CB trails the S&P 500 Financials Sector SPDR (XLF), which recorded a 19.5% gain over the last 52 weeks. Year-to-date, CB has not been able to keep pace with XLF’s 8.8% growth.

Chubb has been struggling to keep pace with the broader market, pressured by a rotation out of defensive stocks, rising competition in property insurance, and persistent macroeconomic headwinds. That weakness resurfaced after the company released its second-quarter results on July 22. Even though the insurer posted strong numbers, shares slipped almost 3.1% the following trading day as investors shrugged off the beat and focused instead on broader market trends.

Net premiums written, a key top-line metric closely watched by insurance investors, rose 6.3% year-over-year (YOY) to $14.2 billion. Core operating EPS for Q2 2025 reached $6.14, surpassing analyst expectations of $5.98 on a non-GAAP basis and marking a 14.1% increase from the previous year. The muted market response had less to do with Chubb’s performance and more to do with the current investment climate. With defensive names out of favor, even a strong quarter wasn’t enough to capture Wall Street’s attention.

Looking ahead, analysts project Chubb’s EPS for fiscal year 2025, ending in December, to decline by 4.2%, reaching $21.57 on a diluted basis. Nevertheless, the company holds an impressive track record of consistently exceeding consensus estimates over the past four quarters.

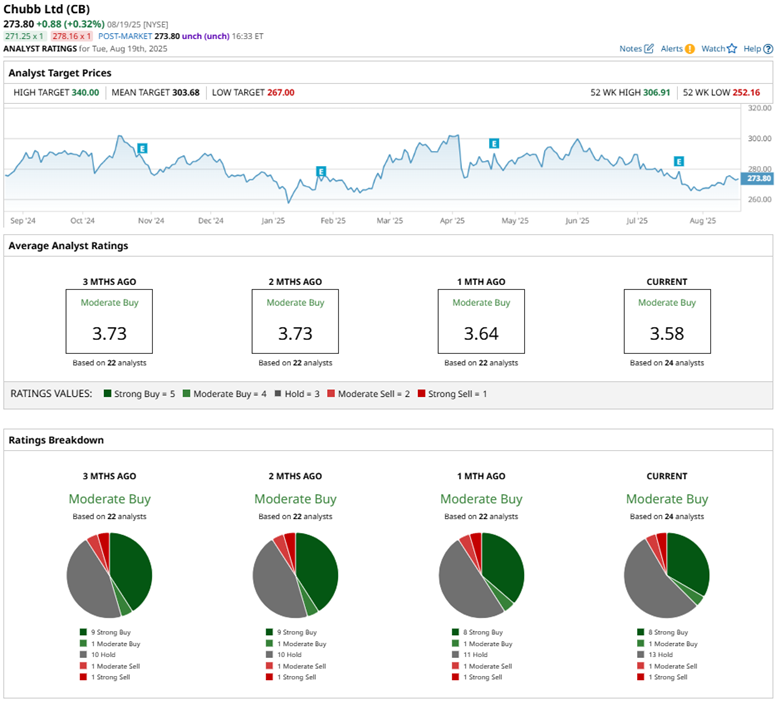

Among 24 analysts covering the stock, the consensus rating is a “Moderate Buy,” comprised of eight “Strong Buy” ratings, one “Moderate Buy,” 13 “Hold” recommendations, one “Moderate Sell,” and one “Strong Sell.”

The current analyst sentiment appears slightly less bullish than it was two months ago, when nine analysts held “Strong Buy” positions, compared to eight.

Despite investors’ lukewarm reaction to CB’s second-quarter results, analysts remain optimistic. For instance, MP Securities reaffirmed its “Market Outperform” rating and maintained a price target of $325, reflecting continued optimism from the Street regarding the company’s performance.

Moreover, on August 13, Citigroup Inc. (C) analyst Matthew Heimermann initiated coverage on CB, assigning a “Buy” rating and setting a price target of $326, signaling confidence in the insurer’s prospects.

The mean price target of $303.68 represents a 10.9% premium to CB’s current price levels. Meanwhile, the Street-high price target of $340 suggests a potential upside of 24.2%.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.